European Sustainability Reporting Standards

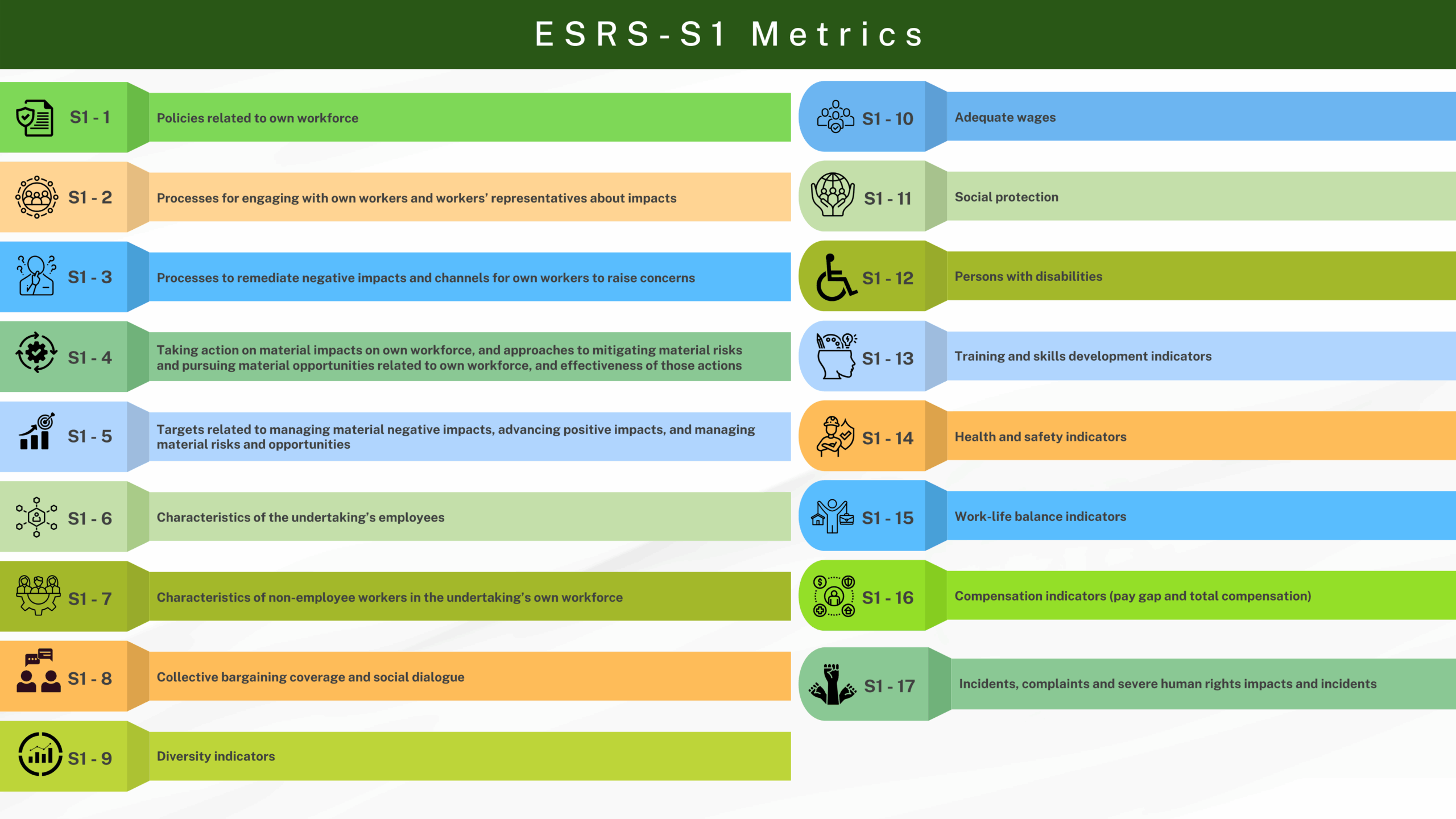

ESRS S1 (European Sustainability Reporting Standards – Social 1) focuses on the disclosure requirements related to an organization’s impact on its workforce. It is a key standard under the Corporate Sustainability Reporting Directive (CSRD) and requires companies to report on 17 specific metrics across four categories:

S1 - 1

Policies related to own workforce

S1 - 2

Processes for engaging with own workers and workers’ representatives about impacts

S1 - 3

Processes to remediate negative impacts and channels for own workers to raise concerns

S1 - 4

Taking action on material impacts on own workforce, and approaches to mitigating material risks and pursuing material opportunities related to own workforce, and effectiveness of those actions

S1 - 5

Targets related to managing material negative impacts, advancing positive impacts, and managing material risks and opportunities

S1 - 6

Characteristics of the undertaking’s employees

S1 - 7

Characteristics of non-employee workers in the undertaking’s own workforce

S1 - 8

Collective bargaining coverage and social dialogue

S1 - 9

Diversity indicators

S1 - 10

Adequate wages

S1 - 11

Social protection

S1 - 12

Persons with disabilities

S1 - 13

Training and skills development indicators

S1 - 14

Health and safety indicators

S1 - 15

Work-life balance indicators

S1 - 16

Compensation indicators (pay gap and total compensation)

S1 - 17

Incidents, complaints and severe human rights impacts and incidents